Commercial General Liability Insurance: A Complete Guide

Running a business always carries risks. Even the most careful business owner can face accidents, injuries, or lawsuits. This is where Commercial General Liability Insurance (CGL) comes in. CGL is one of the most important types of insurance for businesses of all sizes. It protects your company from common risks that could lead to big financial losses.

Imagine a customer slips and falls in your store. Or, your employee accidentally damages a client’s property. These incidents can lead to expensive legal claims. Without protection, a single lawsuit could threaten your business’s survival. CGL insurance gives peace of mind and lets you focus on growing your company.

This guide will help you understand how CGL insurance works, what it covers, what it does not cover, and how to choose the right policy for your business. You’ll also find practical examples, data, and answers to common questions.

What Is Commercial General Liability Insurance?

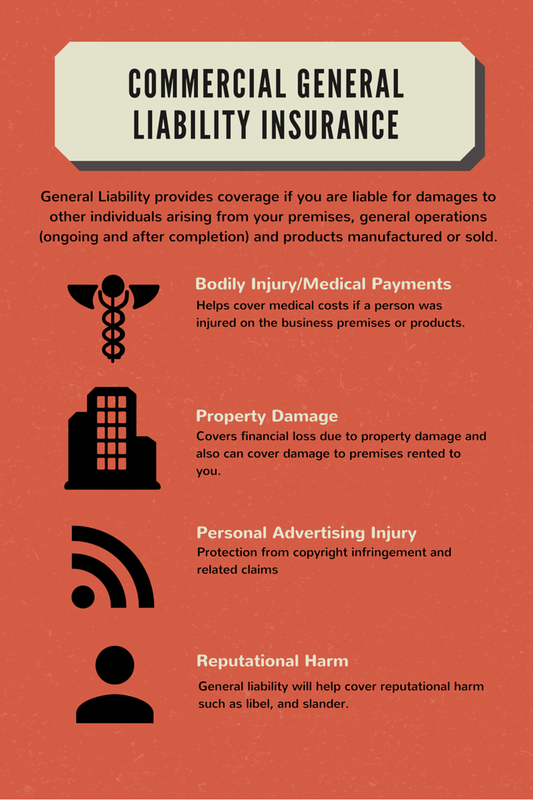

Commercial General Liability Insurance is a policy that covers businesses against claims for bodily injury, property damage, and personal injury. These claims can come from customers, clients, vendors, or even strangers.

If your business is found legally responsible for an incident, CGL insurance helps cover legal costs, settlements, and sometimes medical expenses. In short, it acts as a safety net for many common risks that businesses face every day.

CGL insurance does not cover everything. It focuses on third-party claims, meaning claims from people who do not work for your company. It does not replace other types of insurance like workers’ compensation or professional liability.

Why Is Cgl Insurance Important For Businesses?

Every business, from small shops to large companies, faces risks. Some industries, like construction or retail, face more risks than others. But even office-based businesses can get sued if someone slips and falls.

Here are some reasons why CGL insurance is essential:

- Legal Requirements: Some clients, landlords, or government contracts require you to have CGL insurance.

- Financial Protection: Lawsuits can cost thousands or even millions of dollars. CGL pays for legal defense and settlements.

- Peace of Mind: With insurance, you can focus on your work instead of worrying about unexpected accidents.

- Professional Image: Having insurance shows clients and partners that you are responsible and prepared.

According to the Insurance Information Institute, the average slip-and-fall claim costs over $20,000. Without insurance, many small businesses would not survive such expenses.

What Does Cgl Insurance Cover?

CGL insurance policies cover several types of risks. The main areas are:

Bodily Injury

If a non-employee gets hurt on your business property, CGL can cover their medical bills and your legal costs. For example, a customer trips over a loose carpet and breaks an arm.

Property Damage

If your business activities damage someone else’s property, CGL can pay for repairs or replacement. For example, your delivery driver accidentally backs into a client’s fence.

Personal And Advertising Injury

This covers claims like libel, slander, copyright infringement, or false advertising. For example, if a competitor claims your ad campaign hurt their reputation.

Medical Payments

CGL may cover medical costs for minor injuries, even if you are not legally responsible. This is a goodwill gesture to avoid larger lawsuits.

Here’s a quick comparison of what CGL covers:

| Covered Incident | Example | Is It Covered? |

|---|---|---|

| Customer injury on property | Slip and fall in store | Yes |

| Employee injury | Worker falls from ladder | No (Use workers’ comp) |

| Property damage | Breaks client’s window | Yes |

| False advertising claim | Competitor sues for libel | Yes |

What Does Cgl Insurance Not Cover?

CGL insurance is broad, but not unlimited. It does not cover:

- Employee Injuries: Workers’ compensation insurance is needed.

- Professional Mistakes: Errors in advice or services are covered by professional liability insurance.

- Intentional Acts: Deliberate harm or illegal acts are excluded.

- Auto Accidents: Commercial auto insurance is needed for vehicles.

- Damage to Your Own Property: CGL covers third-party property, not your business assets.

- Contractual Liability: Some contracts require special insurance.

Here is a side-by-side look at CGL vs. other insurance types:

| Insurance Type | Main Coverage | Common Example |

|---|---|---|

| Commercial General Liability | Third-party injury & property damage | Customer slips in store |

| Workers’ Compensation | Employee injuries at work | Worker breaks leg on job |

| Professional Liability | Errors in advice/services | Accounting mistake harms client |

| Commercial Auto | Vehicle-related accidents | Delivery van hits another car |

| Property Insurance | Your building & equipment | Fire damages your office |

Credit: www.thehartford.com

Types Of Cgl Insurance Policies

There are two main types of CGL policies:

Occurrence Policy

This policy covers claims for incidents that happen during the policy period, even if the claim is filed later. For example, if someone is injured in 2023 but files a claim in 2025, you’re still covered if your policy was active in 2023.

Claims-made Policy

This policy only covers claims made while the policy is active. If your policy ends and someone files a claim later, you are not covered unless you buy “tail” coverage.

Most small businesses choose occurrence policies because they provide longer-lasting protection.

How Much Does Cgl Insurance Cost?

CGL insurance costs depend on several factors:

- Business size and industry

- Location

- Annual revenue

- Number of employees

- Claims history

- Coverage limits

The average cost for a small business in the US is $500 to $1,500 per year for $1 million in coverage. High-risk industries like construction or manufacturing pay more, while low-risk businesses like consultants pay less.

Example Premiums

- A retail store pays about $700 per year.

- A construction company may pay $2,500+ per year.

- A home-based consultant may pay as little as $300 per year.

Some policies have deductibles, meaning you pay a small amount before insurance starts paying.

How To Choose The Right Cgl Policy

Choosing the right policy is not always simple. Here are some steps to guide you:

- Assess Your Risks: Think about your business activities. Do customers visit your location? Do you work on other people’s property?

- Check Legal Requirements: Some states or clients require specific coverage amounts.

- Compare Coverage Limits: Common limits are $1 million per claim and $2 million total per year.

- Review Exclusions: Every policy has things it does not cover. Read carefully.

- Ask About Additional Insureds: Some clients will ask to be added to your policy.

- Work With an Agent: An insurance broker can help find the best fit for your needs.

A common mistake is buying the cheapest policy without checking the details. Sometimes, low-cost plans have high deductibles or limited coverage. Make sure the policy fits your actual risks.

Real-world Examples

- A plumbing company accidentally floods a client’s home. The client sues for $40,000 in repairs. CGL insurance pays for the damages and the plumber’s legal fees.

- A café owner faces a lawsuit after a customer slips on a wet floor. The total cost is $25,000. Without CGL insurance, the owner would have to pay from their own pocket.

- A marketing agency gets sued for using a copyrighted image in an ad. CGL helps cover the legal defense and any settlement.

Credit: pi-ins.com

Common Misunderstandings About Cgl Insurance

Even experienced business owners sometimes misunderstand CGL insurance. Here are two things many people miss:

- CGL Does Not Cover Everything: Some owners think CGL is “all-in-one” insurance. In reality, you still need property, auto, or professional liability policies for other risks.

- Claims-Made vs. Occurrence Confusion: Many people do not realize that claims-made policies stop protecting you after the policy ends, while occurrence policies protect against incidents that happened during the policy period, even if the claim comes years later.

Being clear about what your policy covers—and what it doesn’t—can prevent expensive surprises.

How To File A Claim

If something goes wrong, here’s what to do:

- Notify Your Insurer Quickly: Report the incident as soon as possible.

- Document Everything: Take photos, get witness statements, and keep receipts.

- Cooperate with Investigators: Your insurance company will investigate the claim.

- Follow Up: Stay in touch with your agent and insurer about the claim’s progress.

Delaying a claim or giving incomplete information can slow down the process or result in denial.

Credit: www.zimmerinsure.com

Practical Tips For Managing Cgl Insurance

- Review Your Policy Each Year: As your business grows, your risks may change.

- Bundle Policies for Savings: Some insurers offer package deals with property or auto insurance.

- Keep Good Records: Detailed records of incidents, repairs, and safety steps can help if you need to file a claim.

- Train Employees: Teach staff how to prevent common accidents.

- Ask About Discounts: Many insurers give lower rates for businesses with no claims or strong safety programs.

Frequently Asked Questions

What Is The Difference Between Cgl And Professional Liability Insurance?

CGL insurance covers physical injuries and property damage to third parties. Professional liability insurance covers mistakes or negligence in your professional services, such as giving incorrect advice. Many businesses need both types of insurance.

Do I Need Cgl Insurance If I Work From Home?

Yes. Even home-based businesses can face risks. For example, if a client visits your home office and gets injured, you could be sued. Homeowner’s insurance usually does not cover business claims.

How Much Coverage Do I Need?

Most small businesses choose at least $1 million per claim and $2 million total per year. High-risk industries may need more. Your agent can help you decide the right amount based on your risks and contracts.

Can I Add Clients Or Landlords As “additional Insureds”?

Yes. Many clients or landlords require you to add them to your policy. This means your insurance will also protect them if a claim arises from your work. This is a common request in contracts.

Where Can I Learn More About Cgl Insurance?

A great starting point is the Wikipedia page on Commercial General Liability Insurance. It covers the basics and links to reliable resources for further reading.

Protecting your business is not just about profits. It’s about being ready for the unexpected. With the right CGL insurance, you can face challenges with confidence, knowing your business is secure.

Read More:

- Insurance Marketing Strategies 2026: Top Trends to Watch

- Best Insurance Affiliate Programs: Top Picks to Maximize Earnings

- Insurance Software for Agencies: Boost Efficiency and Growth

- Best Health Insurance for Freelancers: Top Plans Compared

- Liability Insurance for Contractors: Essential Protection Guide

- Insurance Policy Management Software: Streamline Your Workflow

- Affordable Burial Insurance Plans: Secure Peace of Mind Today

- Best Travel Medical Insurance Plans: Top Picks for 2024